Finance & Career

Why should I save for my child’s college education? Many parents are wondering how to help their children offset the cost of college or trade school. By saving for your child’s education, you start to achieve the goal of reducing future educational debt and boosting tax benefits.

Why should I save for my child’s college education? Many parents are wondering how to help their children offset the cost of college or trade school. By saving for your child’s education, you start to achieve the goal of reducing future educational debt and boosting tax benefits.

What Are 529 Plans?

There are two types of 529 plans, the college savings plan and the prepaid tuition plan. These plans, offered by most states, can fund education and offer tax benefits. A 529 plan can be used to cover expenses at more than 6,000 United States programs that offer education beyond high school. Qualifying expenses include tuition, room and board, technology items (computer, printer, Internet service), and required books and lab supplies.

College Savings Plans

The most popular 529 plan option is the college savings plan. Your after-tax contributions are invested, which allows more growth than a traditional savings account.

Prepaid Tuition Plans

These plans allow you to pre-pay at the current tuition rate part or all of the private or public college tuition costs and fees for your child’s future education. This plan cannot be used to cover room and board at colleges or universities or to cover tuition at elementary or secondary schools.

What Age Should A Child Be When You Start Saving?

You can begin saving at any age, but you cannot open an account for an unborn child. Parents can, however, open their own 529 account, naming themselves as the beneficiaries, start saving, and add a child as a beneficiary after he or she is born.

Why Should You Start Saving Early?

By beginning to save early, you maximize your gains and spread out the cost of your investment. If a family saves $50 per month from birth to 18 at a 4 percent interest rate, they will have saved $15,779.62. Following the same plan but starting three years before the child’s birth, a family can save $19,697 by the time the child turns 18. You can continue to put money into the account while your child is in college, trade school, or a qualifying program. See the chart below for examples of how money grows over time.

Table 1. Saving from Birth to the Age of 18, You Will Have $15,779.62

| Years | Future Value (4.00%) | Total Contributions |

|---|---|---|

| Year 0 | $0.00 | $0.00 |

| Year 1 | $611.12 | $600.00 |

| Year 2 | $1,247.14 | $1,200.00 |

| Year 3 | $1,909.08 | $1,800.00 |

| Year 4 | $2,597.98 | $2,400.00 |

| Year 5 | $3,314.95 | $3,000.00 |

| Year 6 | $4,061.13 | $3,600.00 |

| Year 7 | $4,837.71 | $4,200.00 |

| Year 8 | $5,645.93 | $4,800.00 |

| Year 9 | $6,487.07 | $5,400.00 |

| Year 10 | $7,362.49 | $6,000.00 |

| Year 11 | $8,273.57 | $6,600.00 |

| Year 12 | $9,221.77 | $7,200.00 |

| Year 13 | $10,208.61 | $7,800.00 |

| Year 14 | $11,235.64 | $8,400.00 |

| Year 15 | $12,304.52 | $9,000.00 |

| Year 16 | $13,416.95 | $9,600.00 |

| Year 17 | $14,574.70 | $10,200.00 |

| Year 18 | $15,779.62 | $10,800.00 |

Table 2. Saving Three Years Before a Child’s Birth, You Will Save $19,697.00

| Years | Future Value (4.00%) | Total Contributions |

|---|---|---|

| Prior Year (1) | $0.00 | $0.00 |

| Prior Year (2) | $611.12 | $600.00 |

| Prior Year (3) | $1,247.14 | $1,200.00 |

| Year 0 | $1,909.08 | $1,800.00 |

| Year 1 | $2,597.98 | $2,400.00 |

| Year 2 | $3,314.95 | $3,000.00 |

| Year 3 | $4,061.13 | $3,600.00 |

| Year 4 | $4,837.71 | $4,200.00 |

| Year 5 | $5,645.93 | $4,800.00 |

| Year 6 | $6,487.07 | $5,400.00 |

| Year 7 | $7,362.49 | $6,000.00 |

| Year 8 | $8,273.57 | $6,600.00 |

| Year 9 | $9,221.77 | $7,200.00 |

| Year 10 | $10,208.61 | $7,800.00 |

| Year 11 | $11,235.64 | $8,400.00 |

| Year 12 | $12,304.52 | $9,000.00 |

| Year 13 | $13,416.95 | $9,600.00 |

| Year 14 | $14,574.70 | $10,200.00 |

| Year 15 | $15,779.62 | $10,800.00 |

| Year 16 | $17,033.63 | $11,400.00 |

| Year 17 | $18,338.73 | $12,000.00 |

| Year 18 | $19,697.00 | $12,600.00 |

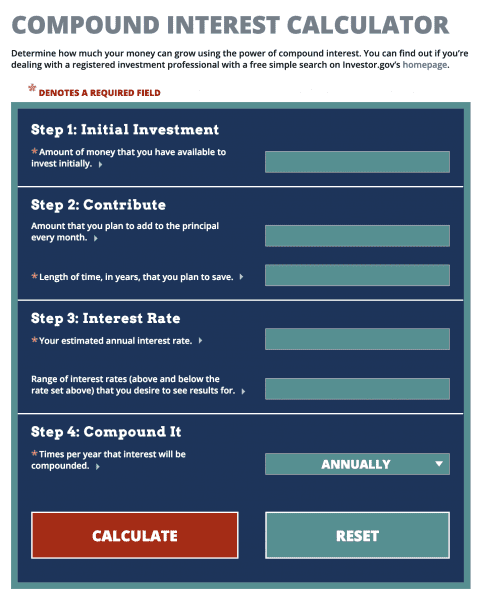

Compounding interest can be determined by using the calculator on the U.S. Securities and Exchange Commission website at https://www.investor.gov/. Find the calculator under Additional Resources.

Compounding interest can be determined by using the calculator on the U.S. Securities and Exchange Commission website at https://www.investor.gov/. Find the calculator under Additional Resources.

You can also use the compounding interest calculator to estimate how much your money will grow. This example in table 1 illustrates opening an investment with $0 (step 1), adding $50 per month with a monthly compounding interest rate of 4 percent. In step 2, you enter the amount of money you plan to contribute each month. Remember, you can use extra money from birthday gifts, extra jobs, and income tax returns to help your money grow even more.

Will Your 529 Investment Be Insured against Loss?

The 529 savings plans are investments that will fluctuate with the market. State governments do not guarantee protection of funds in educational savings. These investments in mutual funds and exchange- traded funds are not federally guaranteed, but investments in some principal-protected bank products may be insured by the FDIC. There may be a risk of financial loss. To better understand the risk, talk with a financial adviser or the state agency that administers the 529 plan. Before opening a 529 account, decide on the type of investment you want for your plan. This might be a mutual fund and exchange-traded fund portfolios and a principal-protected bank product.

How to Open a 529 Account

Go to www.savingforcollege.com. Choose the 529 plans icon at the top of the tool bar.

Scroll down until you see a US map. Select any state to review its 529 plans.

Anyone can open a college savings plan. For example, a parent, grandparent, or other family member can participate. Also, when children turn 18, they can open a 529 account and name themselves as beneficiary.

The social security number of the 529 account beneficiary is required to open an account. The beneficiary is the child who will eventually use the account for eligible expenses. The person who opens the account is called the owner. The owner will be asked to provide his or her name, address, phone number, social security number, and email address. The account owner is the adult who opens the 529 account. Some plans may require you to name another adult who can take over the account in case of your death. This person is called the successor. He or she is someone whom you trust to manage the account for the child. You will need to provide the successor’s name, address, and social security number.

You can fill out an application online or complete a paper application and mail it in. If you have questions, contact the customer service representative for the plan you want to open.

College Savings Plan

Pros

- You can invest in any state’s 529 plan, not just your home state.

- Qualified 529 plan withdrawals do not have to be reported as income on the FAFSA.

- The 529 savings are considered parental assets and will not be counted for more than 5.64 percent on the FAFSA Expected Family Contribution.

- Qualified withdrawals cover any expenses related to school. These include tuition, room and board, books and supplies, and student fees.

Cons

- Nonqualifying withdrawals will be subject to a 10 percent penalty. The original contribution is not taxed, only the earnings portion.

Prepaid Tuition Plans

Pros

- Allows you to pay for future schooling at today’s prices, which may be helpful if tuition increases.

Cons

- Can only be used by residents of the state sponsoring the plan.

- Can only be used for colleges and universities covered by the plan.

- Can usually only be used for tuition, not room and board, books, or other fees.

Federal Tax Benefits

- More than 30 states offer residents a tax deduction or credit for 529 plan contributions

- The IRS considers contributions up to $15,000 per child as gifts.

Alabama Tax Benefits

- Alabama taxpayers can deduct contributions to the CollegeCounts (see resources) Plan for up to $5,000 for single contributors and $10,000 for married contributors, if both are contributing.

Other Things to Consider

Other Things to Consider

- Fees. Most plans have a fee to administer and manage a 529 account. Annual fees vary by state. Some states offer zero-cost plans, and some plans include a fixed maintenance fee. Account owners who opt for electronic deposits and documents may receive fee waivers.

- Direct-sold versus broker-sold plans. Direct-sold plans are sold directly to the investor (you) and do not require a financial adviser. Broker-sold plans are sold through a financial adviser and tend to have higher costs, as you may have to pay the adviser a fee.

- Investment options. Some plans allow you to have more control of the investments, while others change automatically as your child ages. A minimum contribution of $10 is required for some plans, and others require higher contributions. Select a state plan that will help you meet your goal. Remember, tax benefits may be lost if your 529 plan is not in your state of residency. You can view comparison charts at savingforcollege.com.

What if Your Child Decides not to Attend College

- You can make an unqualified withdrawal of the funds, but you will have to pay income tax and a 10 percent penalty

- You change the beneficiary to another family member.

Note: A separate 529 account must be opened for each child.

Resources

Choosing a plan:

Best Plans of 2018

- https://www.savingforcollege.com/intro-to-529s/which-is-the-best-529-plan-available

Plans offered in Alabama

- https://www.collegecounts529.com/529-overview/

Comparing 529 Plans

- https://www.savingforcollege.com/compare_529_plans/

To check if an institution is 529 eligible:

- https://www.savingforcollege.com/eligible_institutions/

General information about 529 Plans:

- https://www.savingforcollege.com/intro-to-529s/what-is-a-529-plan

- https://www.forbes.com/sites/katiepf/2017/10/26/when-it-comes-to-529-plans-parents-just-dont-understand/#7603bca242de

- https://investor.vanguard.com/529-plan/

- https://www.forbes.com/sites/katiepf/2017/10/26/when-it-comes-to-529-plans-parents-just-dont-understand/#7603bca242de

- Consumer Financial Protection Bureau

- https://www.consumerfinance.gov/

- (855) 411-2372

Katrina Akande, Extension Specialist, Assistant Professor, Family and Child Development, and Joelle Smith, Graduate Assistant, Human Development and Family Studies, both with Auburn University

Reviewed December 2021, College Savings: A Parent’s Guide to 529 Plans, FCS-2333