Farm Management

Rising costs of living continue to be a burden for households across Alabama. Results from the 2025 Our State, Our Lives: Alabama Wellbeing Survey1, henceforth referred to as the Our State, Our Lives Survey, show that many residents, especially those with lower incomes, less education, women, and middle-aged adults, struggle to keep up with their regular household bills. Even among groups traditionally viewed as financially stable, such as college graduates, a notable share report experiencing at least occasional financial difficulty in the 12 months preceding the survey. There are also important differences based on where they live. This report summarizes information about retirees and full-time employees who make household financial decisions to provide insight into the financial wellbeing of households across Alabama.

Comparing Rural, Urban & Suburban: Geography Matters

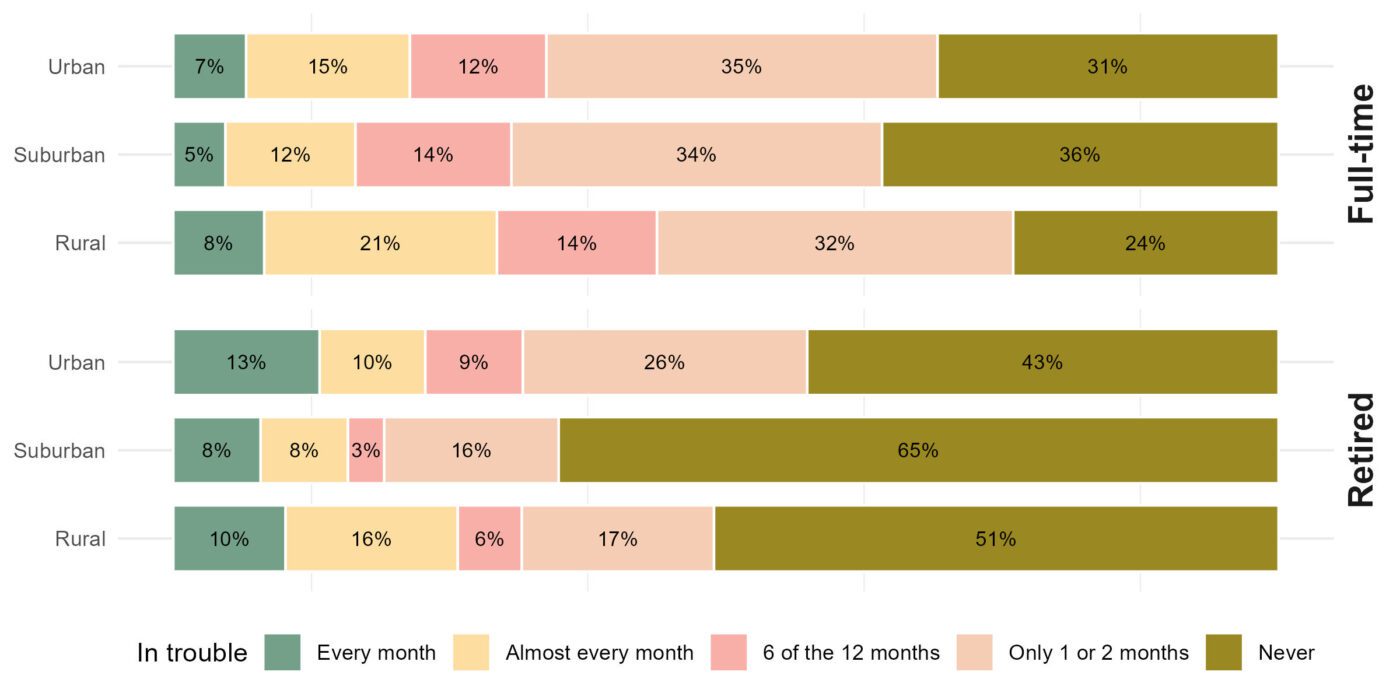

Rural households, especially those with members working full-time, are more likely than suburban or urban households to experience financial strain. According to the “Our State, Our Lives Survey,” 43% of rural full-time workers reported trouble paying bills in at least half of the past 12 months, compared with 34% in urban areas and 31% in suburban areas. Among retirees, 32% of rural respondents said they struggled during at least 6 of the 12 months, compared with 31% of urban and only 19% of suburban retirees (figure 1).

Figure 1. Trouble keeping up with household bills by employment status and place of residence

Gender Matters in Understanding Experiences of Financial Wellbeing in Alabama

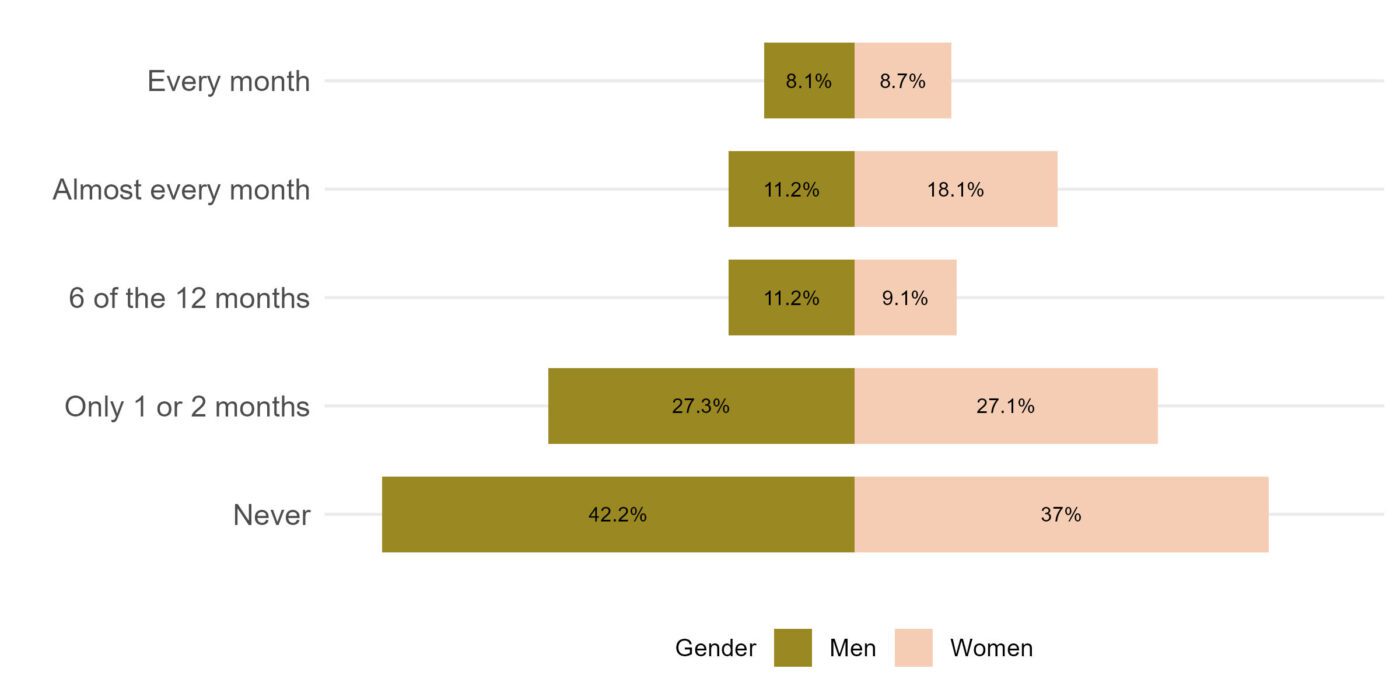

Women report slightly more difficulty keeping up with household bills than men, particularly among the respondents who said they struggled almost every month or every month (figure 2). A higher share of women had trouble almost every month or every month, while a slightly larger share of men said they never experienced difficulty paying their household bills. The gap is most pronounced in the “almost every month” category, where women are 7% higher than men.

Figure 2. Trouble keeping up with household bills by gender

Differences in Financial Wellbeing Vary by Age

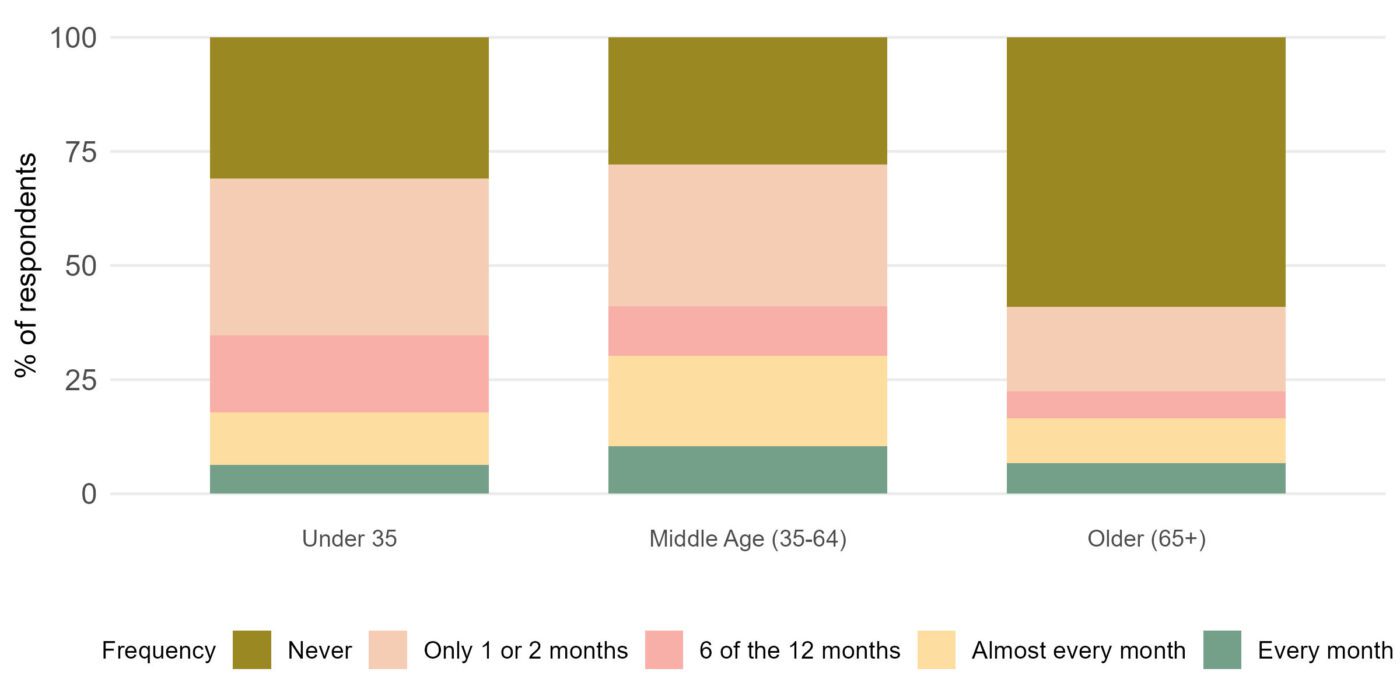

Financial stress tends to ease with age. The share of respondents reporting difficulty paying household bills declines from those under 35 to those 65 and older. However, middle-aged adults stand out as particularly strained. More than four in ten (41%) reported struggling with bills during at least half of the past 12 months, compared with 35% of younger adults and 22% of older adults (figure 3).

Figure 3. Trouble keeping up with household bills by age group

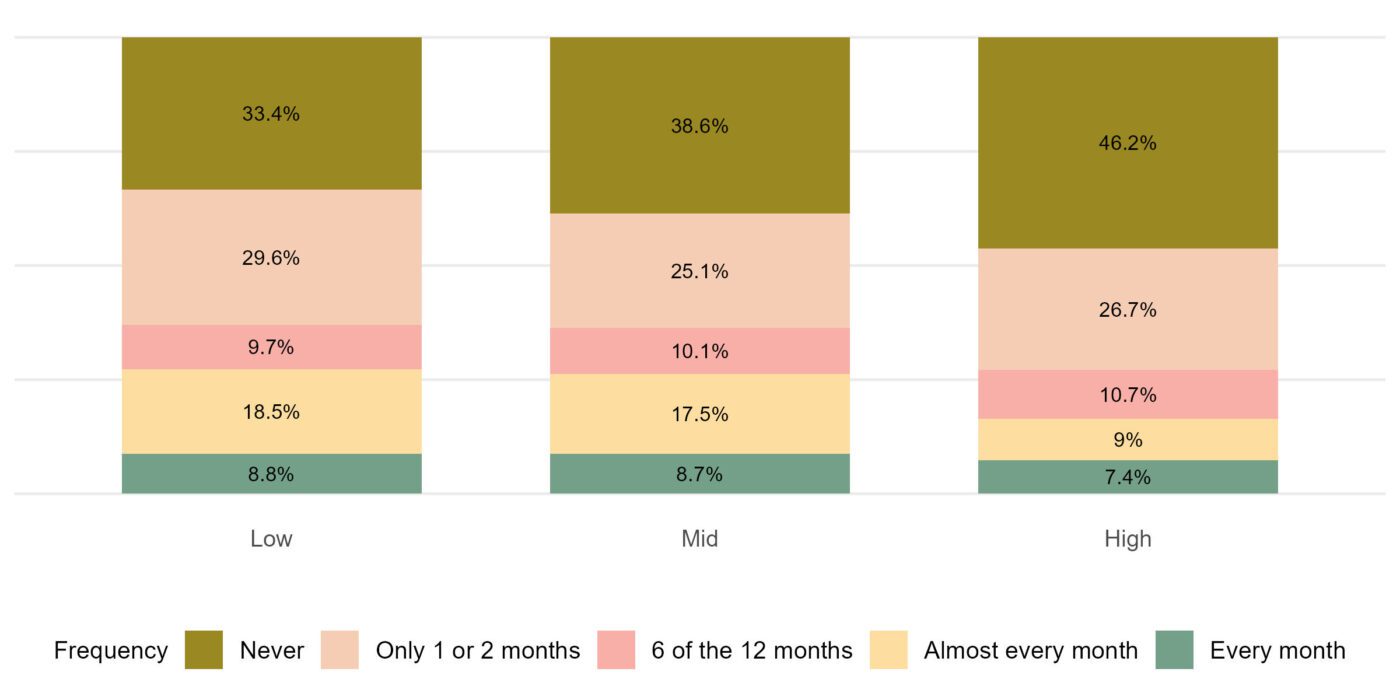

Household Income Matters for Financial Wellbeing

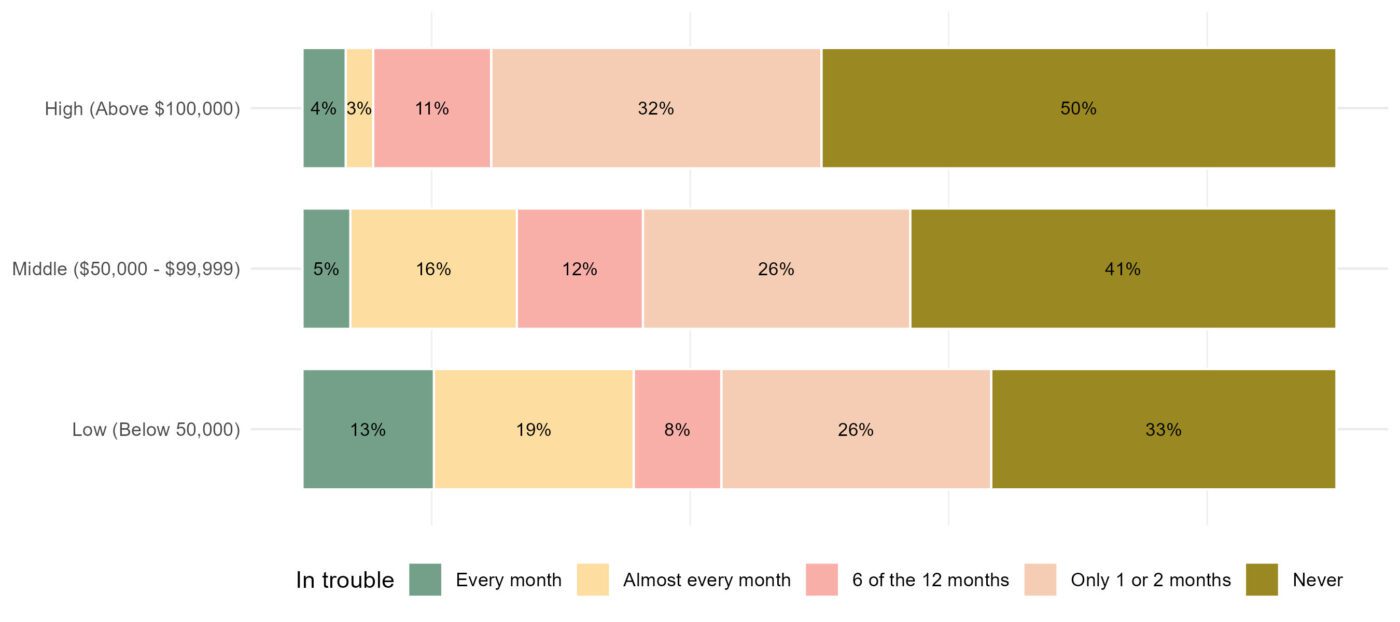

As household income increases, financial stability improves sharply. Only one-third of low-income households report never having trouble paying bills, compared with half of high-income households. More than one in three low-income respondents report frequent or ongoing difficulty (every month or almost every month), compared with 21% in middle-income and just 7% in high-income households (figure 4).

Figure 4. Trouble keeping up with household bills by income categories

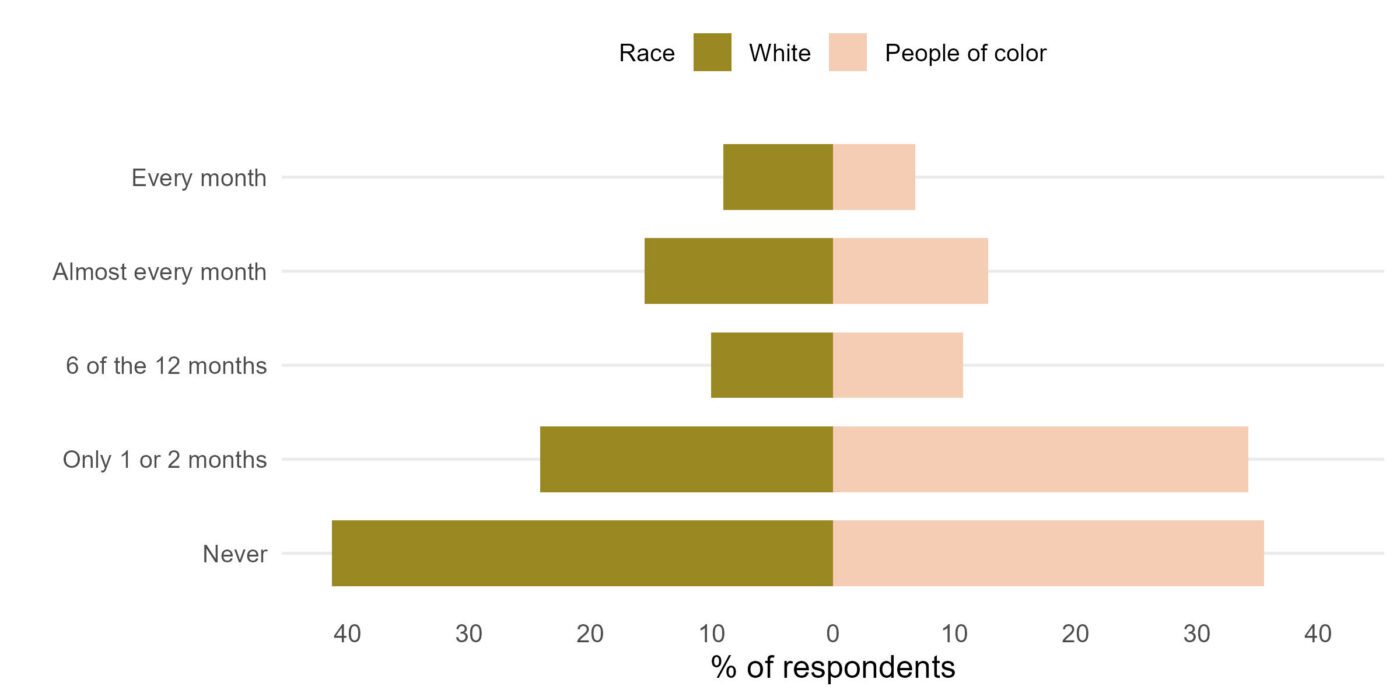

Realities of Financial Wellbeing Differ by Race and Ethnicity

The overall proportion of residents who report any financial strain is similar across groups, but the pattern and consistency of hardship differ. For example, a smaller share of Black, Non-White Hispanic, and Asian respondents reported never struggling to pay household bills compared to White respondents. However, Black, Non-White Hispanic, and Asian residents are more likely to experience occasional difficulty (i.e., reporting strain during only 1 or 2 months). In contrast, White respondents are slightly more likely to report consistent monthly challenges (i.e., almost every month or every month) (figure 5).

Figure 5. Trouble keeping up with household bills by race and ethnicity

Education Attainment Helps Improve Financial Wellbeing, Somewhat

Higher education offers more stability but does not eliminate financial pressure. The share of respondents who said they never had trouble paying bills increases from 34% among those with low education (high school or below) to 47% among highly educated respondents (college degree or above). However, notable proportions across all education levels continue to experience financial difficulties paying their household bills (figure 6).

Figure 6. Trouble keeping up with household bills by education

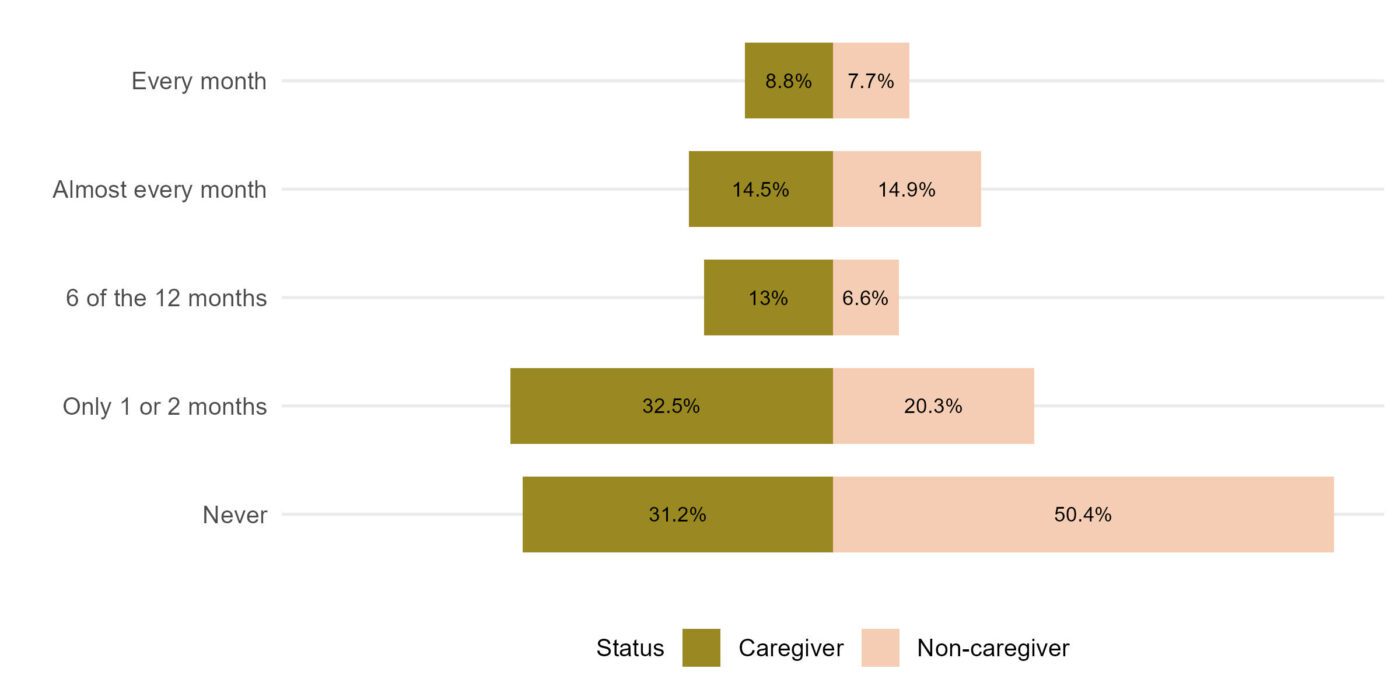

Caregiving Affects Financial Wellbeing

Financial stress is more common among those providing care for others, regardless of who they care for (minors, senior citizens, etc.). Caregivers are less likely to report never having trouble paying bills; only 31% said they never struggled, compared with 50% of non-caregivers. Instead, about one-third of caregivers experienced some financial strain during 1 or 2 months of the past year, and nearly 37% reported difficulty every month during at least half of the past 12-months (figure 7).

Figure 7. Trouble keeping up with household bills by caregiving status

Conclusion

In summary, the 2025 Our State, Our Lives Survey reveals that financial strain remains an important issue across demographic and socioeconomic groups in Alabama, particularly among rural, low-income, younger, and less-educated residents. Even groups traditionally associated with higher stability, such as highly educated or middle- and high-income households, show signs of vulnerability to the rising cost of living.

Citation

1The Our State, Our Lives: Alabama Wellbeing Survey is a biennial survey conducted by the Rural Partnership Institute at Auburn University regarding Alabamians’ wellbeing and quality of life. The survey is conducted online using a best quota sampling frame, meaning that the demographics of the poll reflect the demographics of Alabama regarding age, race, ethnicity, gender, and place (rural, urban, and suburban). The 2025 iteration had 1,947 respondents. This work is supported by the Auburn University Rural Partnership Institute, project award no. 707500-38914, from the US Department of Agriculture’s National Institute of Food and Agriculture. Any opinions, findings, conclusions, or recommendations expressed in this publication are those of the authors and should not be construed to represent any official USDA or US government determination or policy.

Jean R. Francois, Postdoctoral Scholar; Kelli Russell, Assistant Extension Professor; and Mykel R. Taylor, Department Head, Professor, and ALFA Endowed Chair, all in Agricultural Economics and Rural Sociology at Auburn University

Jean R. Francois, Postdoctoral Scholar; Kelli Russell, Assistant Extension Professor; and Mykel R. Taylor, Department Head, Professor, and ALFA Endowed Chair, all in Agricultural Economics and Rural Sociology at Auburn University

New February 2026, Financial Wellbeing Across Alabama: Households Results from 2025 Our State, Our Lives Survey, ANR-3224