Finance & Career

The high cost of everyday goods and services, combined with limited resources, is making it extremely difficult for many individuals and families. The stress and strain of making financial decisions have become a significant challenge for many families when faced with increasing debt and decreasing purchasing power. However, starting the year with good money habits helps families use their money wisely when overcoming economic challenges. When families plan, they can pay their regular bills, prepare for special expenses, and better handle emergencies. In other words, they can learn how to maintain financial discipline during financial challenges.

Budgeting is the process of creating a plan for how you will spend your money. It is also a strategy that can and should be used to help maintain financial discipline during financial challenges. The spending plan, also known as a budget, is a tool used to help families and individuals control wasteful spending by tracking the money coming into a household and the money going out. It helps families manage their limited resources and prevents overspending. Budgeting has also been found to reduce financial stress and strengthen family relationships.

Household Budget Planning

A spending plan works best when all family members are involved in its development and implementation. This tool helps individuals and families establish boundaries and make informed decisions. As with any planning, budget planning involves thinking ahead to set goals, determining the best actions to take, and organizing resources to achieve desired financial outcomes. Three key aspects of household budget planning are expense tracking, setting financial goals, and creating a spending plan or budget.

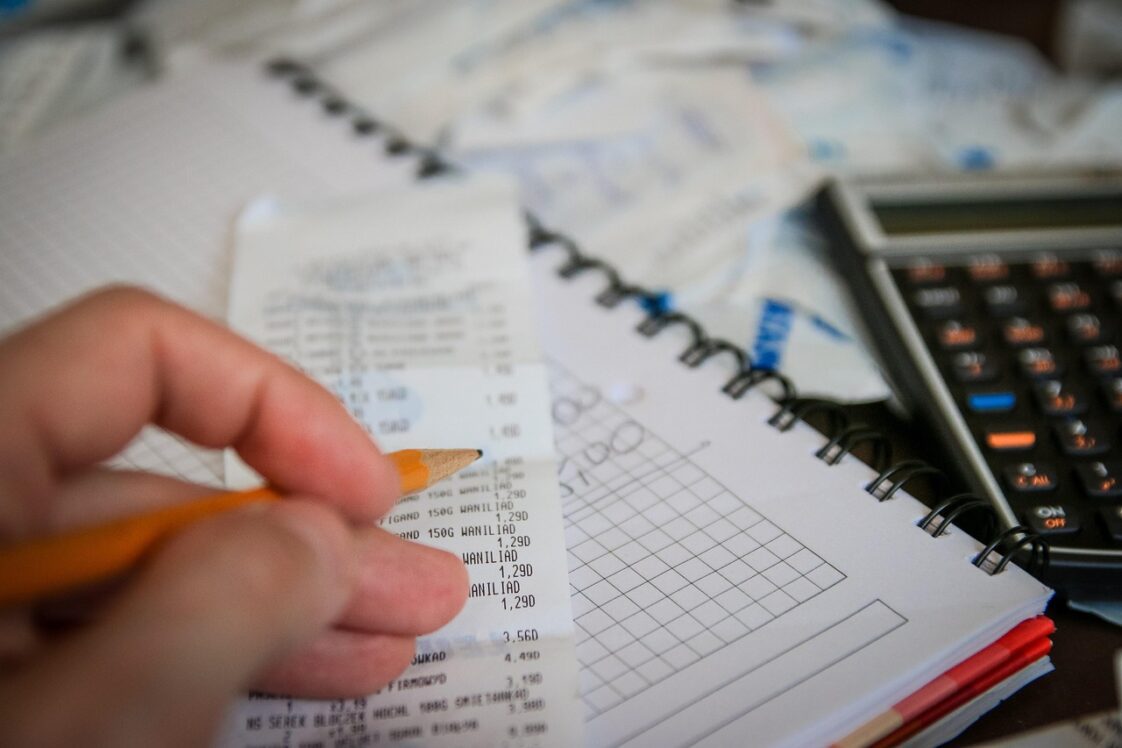

Expense Tracking

Track your spending before creating a budget or establishing goals. Expense tracking, an organized process of how money is spent over time, provides a realistic picture of your financial behavior. This process helps individuals and families to see where their money goes, as well as identify their spending patterns. Tracking spending provides the data needed to determine budget categories. The data obtained shows where overspending is occurring. Knowing where your money is going will not only enhance your financial decision-making but also increase your confidence in managing finances more effectively.

Establish Financial Goals

Family financial goals help individuals and families plan for their financial future. They provide direction and purpose by allowing family members to know what they are saving toward and where or what they are spending their money on. Having clear financial goals increases the likelihood of families saving money and creating and using a budget. Establishing financial goals also helps families make more informed choices by focusing on what is truly important.

Consider existing financial obligations by using data obtained from expense tracking. Decide what is most important to the family, and prioritize them based on the family’s needs. For example, paying the mortgage is more important than going to Disney World. Likewise, establishing an emergency fund before pursuing your financial goals is essential, as it protects the family from unexpected expenses.

Goal setting requires family members not only to align their goals with their values but also to take a long, hard look at their future income and the amount they will need to achieve their established goals within a specific time frame. Goals are usually grouped based on a span of time: short-term (up to 1 year), intermediate (1 to 5 years), and long-term (more than 5 years). When developing individual or family financial goals, ensure they are specific, measurable, attainable, relevant, and time-bound (SMART). Establishing financial goals fosters financial discipline by teaching patience and sound money management habits.

Create a Spending Plan

Just as you plan for so many other things in your life, you must plan how your money should be spent. Regardless of whether you or your family are wealthy or not, everyone needs to create and use a budget. A spending plan is a tool that helps you and your family control and manage your money in an organized and rational manner. It increases the likelihood of achieving financial goals.

To create a spending plan, first, identify and list all sources of income. Second, list and categorize all expenses (fixed and variable). Lastly, earmark income for each expense category. For both income and expenses, use projected figures and actual figures. For example, at the beginning of the month, record the amount of income you project to have coming into the household (income) and record the amount of money you project will be spent under each expense category. Remember, expenses (projected and actual) should not exceed your income (projected and actual). At the end of the budget period, compare your actual spending to your projected spending. Adjust your spending plan as needed.

Summary

Starting the year with good money habits helps you and your family to not only establish financial stability but also family well-being. Financial discipline reduces stress while strengthening family relationships. An important part of financial discipline is budgeting—the process of creating a plan for how you will spend your money. Budgeting involves tracking expenses, establishing financial goals, and establishing a spending plan or budget. Learning these three skills can help individuals and families stay in control of their money, avoid overspending, pay for what they need while saving for the future, make more informed choices, and become more resilient.